Introduction

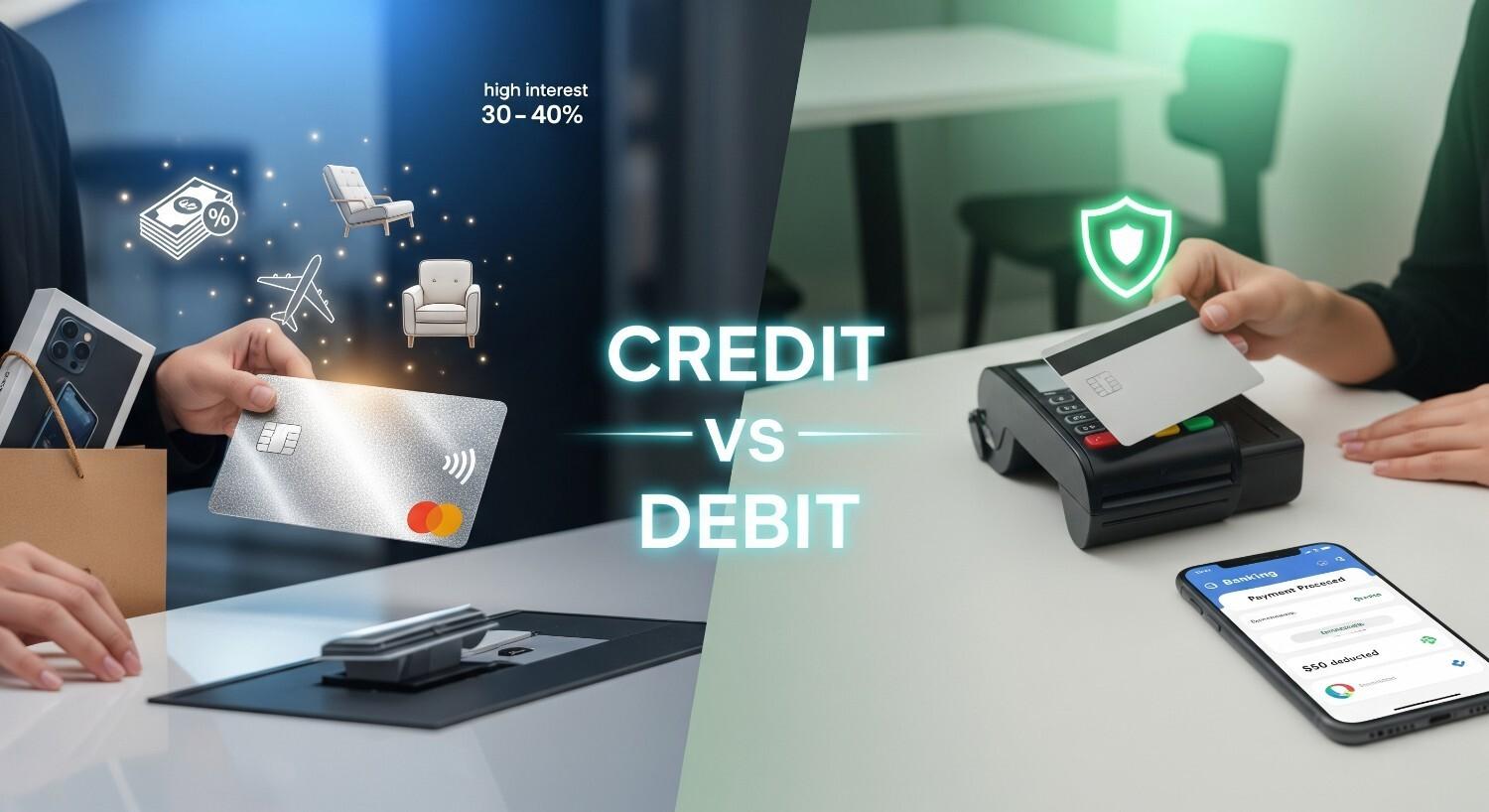

Let’s be honest — the way we handle money today looks nothing like it did ten years ago. Remember when most of us carried cash and worried about whether the shopkeeper had enough change? Fast forward to 2025, and hardly anyone wants to deal with cash anymore. Now, a quick tap, swipe, or scan is all it takes. But even though the world is moving toward UPI apps, digital wallets, and contactless payments, two old companions still sit quietly in almost every wallet: the credit card and the debit card. At first glance, they’re identical pieces of plastic (or sometimes shiny metal, if you’ve got one of those premium ones). Same size, same chip, same swipe. But here’s the twist: the money you’re using is coming from a very different place depending on which one you pick. With a credit card, you’re telling the bank, “Cover me for now, I’ll pay you later.” With a debit card, you’re saying, “Take it directly from my account right away.” That one difference decides everything — whether you get cashback or not, whether your credit score grows or stays flat, and whether you sleep peacefully or stress over debt. Now, people love to argue about credit card vs debit card — which one is better? Some of my friends won’t stop bragging about the rewards they earn on their credit cards. Others refuse to even touch a credit card, saying it’s a trap. And honestly? Both sides are right in their own way. The real question isn’t just which is better overall — it’s which is better for you in 2025.

That’s exactly what we’ll figure out in this blog. I’ll walk you through how each card works, what’s good, what’s risky, and how the financial world around them has changed in 2025. By the end, you won’t just know the textbook differences — you’ll know how to actually use these cards smartly in real life.

What Exactly is a Credit Card?

Imagine this: you’re at the mall and spot a phone you’ve been wanting for months. Price tag? $600. You glance at your account balance — only $130 left till salary day. If you pull out your debit card, game over. Transaction declined. But with a credit card? Boom. Approved. You walk out with that shiny new phone today and worry about paying for it later. That’s the basic idea of a credit card. It’s not your money you’re spending; it’s the bank’s money. They’re lending it to you with the expectation that you’ll pay it back within a set period (usually around 30–45 days). If you pay the full amount on time, you walk away clean. If you don’t, that’s when the interest charges kick in — and trust me, they aren’t small. In 2025, many banks are still charging 30–40% annual interest on unpaid balances. That’s like buying your phone twice if you keep delaying payments. But it’s not all scary. Credit cards can be incredibly rewarding if you play your cards right (pun intended). You get cashback on everyday expenses like groceries and fuel, discounts on flights and hotels, free lounge access at airports, even extra warranties on electronics. Some cards literally pay you to spend money — as long as you’re disciplined enough to clear the bill every month.

The flip side? A credit card is like fire. Keep it under control, and it lights up your life. Lose control, and it burns everything down. Many people fall into the trap of “just paying the minimum due” each month. It feels easy in the moment but slowly turns into a debt spiral that’s hard to escape.

So, in simple words: a credit card is freedom mixed with responsibility. If you’re the kind of person who can manage money carefully, it can actually save you money and open doors to financial opportunities. But if you struggle with discipline, it can become the costliest piece of plastic in your wallet.

What About a Debit Card?

Now let’s flip the coin. Say you’re out for dinner with friends, the bill comes to $50, and you swipe your debit card. Instantly, the money leaves your bank account. No borrowing, no interest, no “I’ll pay later.” What you see is what you spend.

That’s the beauty of debit cards. They keep you grounded. You can’t spend what you don’t have (unless you have overdraft protection, but let’s keep that aside for now). For people who want to avoid debt, debit cards are like a financial safety net.

The other advantage? Debit cards are super simple. No annual fees in most cases, no worrying about interest rates, no risk of overspending beyond your account balance. If you’re someone who likes to keep life straightforward, a debit card quietly does its job without drama.

But debit cards have their downsides too. You don’t really get big rewards. Most banks in 2025 still offer very limited perks on debit cards compared to credit cards. No fancy airport lounges, no huge cashback percentages, no chance of building a credit history. And in today’s financial world, not building a credit score can be a missed opportunity, especially if you ever want to take out a loan for a house, car, or even a business.

So, think of debit cards as the safe option. They’re like a trustworthy old friend who won’t excite you with surprises but also won’t drag you into trouble.

Key Differences Between Credit and Debit Cards in 2025

By now you probably get the general idea, but let’s break it down clearly.

- Source of Money

- Credit card: Bank’s money (loan).

- Debit card: Your own money.

- Payment Timing

- Credit card: Pay later (billing cycle + grace period).

- Debit card: Pay instantly (deducted from account).

- Rewards & Perks

- Credit card: Cashback, discounts, miles, lounge access.

- Debit card: Limited or no rewards.

- Credit Score Impact

- Credit card: Helps build or damage credit score depending on usage.

- Debit card: No impact on credit score.

- Risk Factor

- Credit card: Risk of overspending and high interest debt.

- Debit card: Safer, but limited benefits.

Why Credit Cards Shine in 2025

The year 2025 is different from a few years ago. Banks, fintech companies, and even airlines are competing hard to make their credit cards attractive. Here’s why credit cards feel extra powerful today:

- Better Rewards – Many credit cards in 2025 offer up to 5–6% cashback on categories like dining, online shopping, or travel. That means if you’re spending $1,000 a month, you could easily earn back $50–60 without doing anything extra.

- BNPL Culture – Buy Now, Pay Later has become normal. Credit cards already work like this, and many now integrate directly with BNPL platforms, giving users flexible repayment options.

- Travel Benefits – If you travel often, a credit card is almost a must. Free lounge access, extra baggage allowance, and travel insurance are standard perks now.

- Building Credit History – In 2025, having a solid credit score is more important than ever. Whether it’s getting approved for a mortgage, car loan, or even a job in some industries, your credit report can play a role. Debit cards can’t help here, but credit cards can.

If credit score feels confusing, don’t worry — I’ve shared simple money-saving tips in my blog [How to Save Money Fast on a Low Income] which can give you a strong foundation.

Why Credit Cards Shine in 2025

The year 2025 is different from a few years ago. Banks, fintech companies, and even airlines are competing hard to make their credit cards attractive. Here’s why credit cards feel extra powerful today:

- Better Rewards – Many credit cards in 2025 offer up to 5–6% cashback on categories like dining, online shopping, or travel. That means if you’re spending $1,000 a month, you could easily earn back $50–60 without doing anything extra.

- BNPL Culture – Buy Now, Pay Later has become normal. Credit cards already work like this, and many now integrate directly with BNPL platforms, giving users flexible repayment options.

- Travel Benefits – If you travel often, a credit card is almost a must. Free lounge access, extra baggage allowance, and travel insurance are standard perks now.

- Building Credit History – In 2025, having a solid credit score is more important than ever. Whether it’s getting approved for a mortgage, car loan, or even a job in some industries, your credit report can play a role. Debit cards can’t help here, but credit cards can.

If credit score feels confusing, don’t worry — I’ve shared simple money-saving tips in my blog [How to Save Money Fast on a Low Income] which can give you a strong foundation.

Credit Card vs Debit Card: Which is Better in 2025?

Now comes the million-dollar question: which one is better? The truth is, neither card is “the winner.” It depends on your personality, lifestyle, and financial goals.

- If you’re disciplined, pay bills on time, and love maximizing benefits → Credit card wins.

- If you want simplicity, hate debt, and prefer stress-free money management → Debit card wins.

For most people, the real sweet spot in 2025 is using both together. Keep a debit card for day-to-day expenses where you don’t care about rewards, and a credit card for big purchases, travel, or bills where cashback and perks actually matter. Want to dive deeper into managing your daily expenses? I recently wrote about [Best Budgeting Apps in USA 2025] that can help you organize both your credit and debit card spending.

Bonus: Home Depot Card in 2025 – Is It Worth It?

Now, while we are comparing credit cards and debit cards, it’s also worth talking about something many U.S. shoppers use — the Home Depot Card. This is a store credit card offered by Home Depot, mainly for people who shop there often for home improvement, furniture, or tools.

Here’s how it works: unlike a normal debit card, the Home Depot Card is basically a credit card but limited to Home Depot purchases. You can’t use it everywhere like a Visa or Mastercard. Instead, it’s designed to give you special perks at Home Depot stores, such as:

- Exclusive financing offers: For example, 0% interest if you pay off within 6 months on big purchases.

- Discounts and promotions: Seasonal deals only for cardholders.

- Large purchase management: Helpful if you’re renovating your home and don’t want to pay everything upfront.

But here’s the catch: if you don’t pay off the balance on time, the interest rates can be very high — often much higher than regular credit cards. That’s why the Home Depot Card should be treated carefully, just like any other credit card.

So is it better than a regular credit or debit card?

Not really — it’s more like a specialized tool. If you shop at Home Depot frequently, this card can save you money and give flexibility. But if you’re someone who only visits once in a while, a regular cashback or rewards credit card will be much more useful.

Final Thoughts

Money management in 2025 is all about balance. A credit card can open doors to rewards, comfort, and financial growth, but only if you respect its power. A debit card keeps you grounded and safe but won’t push your finances forward in terms of credit building.

So instead of asking, Which is better — credit or debit?, ask yourself, Which one fits my habits right now? If you can manage discipline, grab a credit card and use it wisely. If not, stick to your debit card until you build better money habits.

At the end of the day, it’s not the card that decides your financial health — it’s how you use it.

At the end of the day, choosing between a credit card and a debit card depends on your lifestyle. But if you want to explore more money hacks, you can read my blog on [How to Start a Dropshipping Business] which shows another way to manage and grow money online.